personality-tests

Big Five Personality and Financial Decisions

How the Big Five personality traits shape financial decisions, risk tolerance, savings habits, and debt management with practical trait-matched strategies.

Quick answer

How do personality traits affect financial decisions?

Conscientiousness is the strongest positive predictor of financial success, driving disciplined saving and higher net worth. Neuroticism promotes risk aversion, extraversion increases overconfidence and trading volume, openness raises risk tolerance, and agreeableness favors conservative family-focused choices.

Source: University of Georgia, Family and Consumer Sciences Research

Key Takeaways

- Conscientiousness is the most powerful personality predictor of wealth accumulation, savings discipline, and long-term financial well-being.

- Neuroticism drives risk aversion and preference for safer investments, sometimes at the cost of growth.

- Extraversion increases risk tolerance and trading activity but also fuels overconfidence bias.

- Openness correlates with higher risk tolerance and interest in volatile assets like stocks and alternative investments.

- Agreeableness leads to conservative, family-security-focused financial choices.

- Personality traits do not operate in isolation. They interact with financial literacy, behavioral biases, and demographic factors.

- Your personality does not determine your financial destiny. Awareness of trait-driven tendencies enables better decision-making.

For a broader look at how personality shapes decision-making processes, see our decision-making styles guide.

Disclaimer: This article summarizes behavioral finance research for educational purposes. It is not personalized financial advice. Consult a licensed financial advisor before making investment decisions.

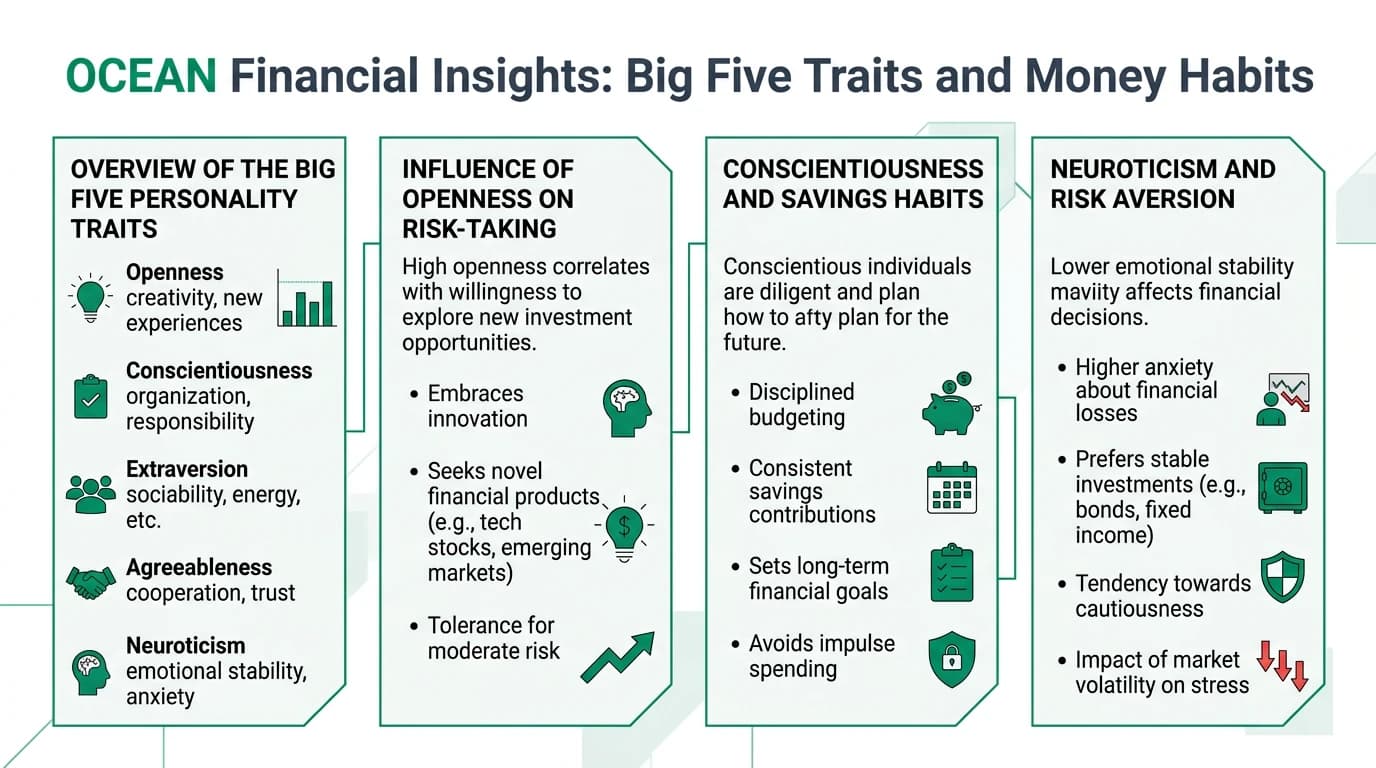

The Big Five and Financial Behavior: An Overview

Each Big Five trait influences a different aspect of financial decision-making. The table below maps traits to their primary financial effects based on multiple research sources.

| Trait | Primary Financial Influence | Risk Tolerance | Savings Behavior | Wealth Impact | Key Bias |

|---|---|---|---|---|---|

| Conscientiousness | Disciplined planning and spending | Moderate (avoid excess) | Strong saver | Positive (highest net worth) | Under-risking |

| Neuroticism | Anxiety-driven avoidance | Low | Inconsistent (stress spending) | Mixed (safety at cost of growth) | Loss aversion |

| Extraversion | Social influence and overtrading | High | Variable | Mixed (gains from action, losses from overtrading) | Overconfidence |

| Openness | Novelty-seeking in investments | High | Variable | Positive (innovative choices) | Optimism bias |

| Agreeableness | Family-focused conservatism | Low to moderate | Moderate | Neutral to positive | Herd behavior |

- Conscientiousness carries the highest weight in regression models predicting financial literacy and outcomes1.

- Personality traits explain financial behaviors that traditional economic models label as "irrational"2.

- Traits influence decisions both directly and indirectly through their effect on financial literacy1.

Conscientiousness and Wealth Accumulation

Conscientiousness is the trait most consistently linked to positive financial outcomes. Highly conscientious individuals save more, spend less impulsively, manage debt better, and accumulate greater net worth over time.

How Conscientiousness Builds Wealth

- Spending discipline reduces impulsive purchases and unplanned expenses.

- Routine adherence supports consistent savings contributions.

- Goal-directed behavior translates into long-term financial planning.

- Lower trading frequency avoids the transaction costs and emotional decisions that erode returns1.

Research from the University of Georgia found that high conscientiousness links to financial happiness over time, potentially because disciplined spending offsets the growth drag of moderate risk-aversion2.

Conscientiousness Financial Profile

| Financial Behavior | Conscientious Individual | Less Conscientious Individual |

|---|---|---|

| Monthly savings rate | Consistent (often automated) | Irregular or absent |

| Impulse purchases | Rare | Frequent |

| Credit card debt | Low, paid in full | Revolving balance likely |

| Emergency fund | Maintained | Under-funded |

| Investment strategy | Buy-and-hold, diversified | Reactive, trend-chasing |

| Retirement planning | On track | Delayed or absent |

- A Federal Reserve Bank of Boston study found that low conscientiousness increases the probability of revolving credit card debt by 7.7 percentage points after controlling for age and income3.

- Conscientiousness also reduces susceptibility to the gambler's fallacy and other cognitive biases that distort financial planning4.

Strategies for Less Conscientious Individuals

You do not need to be naturally high in conscientiousness to build better financial habits. External systems can compensate:

- Automate savings by setting up transfers on payday before discretionary spending is possible.

- Use spending alerts that notify you when purchases exceed a threshold.

- Implement the 24-hour rule: wait a full day before any non-essential purchase over a set amount.

- Schedule monthly financial reviews on a fixed calendar date.

- Use visual tracking (charts, progress bars) for savings goals.

For strategies on how personality influences stress and coping, which directly affects financial decision quality, see our dedicated guide.

Neuroticism and Risk Aversion

Neurotic individuals experience uncertainty as genuinely painful. In financial contexts, this translates to preference for safer investments, lower portfolio volatility, and avoidance of decisions with ambiguous outcomes.

The Neuroticism-Finance Connection

- Risk aversion leads to over-allocation to bonds, savings accounts, and guaranteed-return products.

- Loss aversion makes potential losses feel two to three times more impactful than equivalent gains.

- Anxiety under market volatility triggers panic selling at market bottoms.

- Avoidance behavior may delay important decisions like retirement planning or insurance review.

| Financial Aspect | High Neuroticism Pattern | Potential Cost | Mitigation |

|---|---|---|---|

| Asset allocation | Over-weighted in cash and bonds | Lower long-term returns | Age-appropriate target-date funds |

| Market downturns | Panic selling | Locks in losses | Pre-committed investment policy |

| Decision delays | Avoids financial planning conversations | Missed compounding | Scheduled quarterly reviews |

| Emergency behavior | Stress spending during anxiety peaks | Budget disruption | Separate "stress fund" account |

| Insurance | Over-insured for low-probability events | Premium drag | Risk-probability education |

- Neuroticism negatively impacts both risk tolerance and financial planning outcomes across multiple studies41.

- However, moderate neuroticism can be adaptive: it motivates maintaining emergency funds and avoiding truly reckless risk.

- Understanding your neuroticism level helps distinguish between protective caution and growth-limiting fear. Our neuroticism interpretation guide covers this distinction in depth.

Extraversion and Investment Overconfidence

Extraverts bring energy, social engagement, and proactive decision-making to their finances. The downside is a documented tendency toward overconfidence, excessive trading, and social-influence-driven investment choices.

How Extraversion Affects Investing

- Higher risk tolerance supports growth-oriented portfolios.

- Proactive money allocation means extraverts are more likely to invest rather than leave cash idle.

- Overconfidence bias leads to excessive trading, which erodes returns through transaction costs.

- Social influence susceptibility makes extraverts more likely to chase trending investments discussed in their social networks.

| Bias Type | Link to Extraversion | Financial Impact | Prevention Strategy |

|---|---|---|---|

| Overconfidence | Strong | Overtrading, excessive risk | Set maximum monthly trade limits |

| Availability bias | Moderate | Over-weighting recent news | Use systematic rebalancing schedules |

| Herd behavior | Moderate | Chasing social media trends | Document investment thesis before buying |

| Anchor bias | Moderate | Fixation on purchase price | Focus on fundamentals, not entry point |

- Extraversion significantly relates to risk tolerance and biases like overconfidence across regression studies4.

- Extraverted investors tend to trade more frequently, but higher trading volume is correlated with lower net returns in most research41.

- For insight into how personality drives broader consumer behavior, see our consumer psychology guide.

Strategies for Extraverted Investors

- Automate portfolio rebalancing to remove emotional decision-making from the process.

- Set a "cooling off" rule: discuss any new investment idea with a trusted advisor before acting.

- Track your trades and review quarterly whether frequent trading added or subtracted value.

- Diversify information sources beyond social circles to reduce herd-driven decisions.

Openness and Financial Risk-Taking

People high in openness to experience are drawn to novelty, complexity, and unconventional ideas. In finance, this manifests as higher risk tolerance, interest in alternative investments, and willingness to explore volatile asset classes.

Openness Financial Profile

| Financial Behavior | High Openness | Low Openness |

|---|---|---|

| Investment style | Growth-oriented, alternative assets | Conservative, traditional instruments |

| Risk tolerance | Higher than average | Lower to average |

| New financial products | Early adopter | Skeptical, late adopter |

| Portfolio diversification | Broad (stocks, crypto, ventures) | Narrow (bonds, savings, real estate) |

| Financial literacy engagement | High (curious, reads widely) | Low to moderate |

- Risk-tolerant groups show a mean openness score of 3.18 (on a 5-point scale) compared to lower scores in risk-averse groups4.

- Openness facilitates financial literacy acquisition because curious individuals seek out financial education more actively4.

- The risk is optimism bias: high-openness investors may underestimate downside risk in novel investments.

| Risk Factor | Trigger | Real-World Example | Mitigation |

|---|---|---|---|

| Novelty attraction | New asset class hype | Overconcentration in cryptocurrency | Cap alternative assets at a fixed portfolio percentage |

| Optimism bias | Enthusiasm for innovative companies | Ignoring fundamentals of speculative stocks | Require written risk assessment before investing |

| Complexity seeking | Multi-layered financial products | Losses from poorly understood derivatives | Only invest in products you can explain simply |

Agreeableness and Conservative Financial Choices

Agreeable individuals prioritize harmony, cooperation, and family security. Their financial decisions reflect these values through conservative asset allocation and security-focused planning.

How Agreeableness Shapes Money Decisions

- Family-first prioritization means savings goals center on children's education, home ownership, and emergency readiness rather than aggressive wealth growth.

- Risk avoidance protects capital but may limit returns over long time horizons.

- Financial satisfaction tends to be higher among agreeable individuals because their goals align with achievable security benchmarks rather than aspirational wealth targets5.

- Susceptibility to social pressure can lead to lending money they cannot afford or co-signing loans out of kindness.

| Income Level | Prevalent Trait Pattern | Dominant Financial Priority | Decision Style |

|---|---|---|---|

| Lower income | Higher agreeableness | Security and basic needs | Ultra-conservative |

| Middle income | Balanced agreeableness | Family security and education savings | Moderate, planned |

| Higher income | Variable agreeableness | Diversified but still security-anchored | Conservative with growth allocation |

- Research with Indonesian respondents found that among those earning more than IDR 20 million, agreeableness was the prevalent trait, driving security-focused financial decisions1.

- Agreeableness mediates the relationship between personality and financial satisfaction, suggesting that agreeable people derive contentment from financial security even at lower wealth levels5.

Personality Traits and Financial Literacy

The relationship between personality and financial decisions is not always direct. Financial literacy acts as a mediator, with personality traits influencing how much financial knowledge individuals acquire and how they apply it.

| Literacy Factor | Dominant Trait Predictor | Regression Weight | Mechanism |

|---|---|---|---|

| Investment risk knowledge | Conscientiousness | Highest (0.65) | Systematic study of options |

| General financial awareness | Openness | Moderate | Curiosity-driven learning |

| Practical application | Extraversion | Moderate | Proactive engagement with advisors |

| Perceived literacy (vs. actual) | Extraversion, openness | Moderate | Confidence in financial knowledge |

| Avoidance of financial education | Neuroticism | Negative | Anxiety about financial topics |

- Partial least squares analysis shows that conscientiousness has the highest weight in personality-financial literacy models, followed by openness1.

- Traits affect decisions both directly (e.g., impulsive spending) and indirectly through literacy (e.g., not understanding compound interest)1.

- Overgeneralizing from small samples is a common error. Mean risk tolerance across studies is 3.10 (SD = 0.44) on a 5-point scale, indicating moderate average risk tolerance with substantial individual variation4.

Personality-Driven Behavioral Biases in Finance

Every investor carries cognitive biases. Personality traits predict which biases you are most vulnerable to.

| Cognitive Bias | Primary Trait Link | How It Manifests | Financial Cost | Countermeasure |

|---|---|---|---|---|

| Overconfidence | Extraversion | "I can time the market" | Excessive trading, transaction costs | Automated rebalancing |

| Loss aversion | Neuroticism | "I cannot afford to lose anything" | Under-investing, missed growth | Pre-committed allocation targets |

| Gambler's fallacy | Low conscientiousness | "It crashed, so it must bounce back" | Buying into falling assets | Evidence-based decision framework |

| Availability bias | Extraversion | "Everyone is buying this stock" | Herding into popular assets | Systematic screening criteria |

| Status quo bias | High agreeableness | "My current plan is fine" | Failing to optimize | Annual portfolio review calendar |

| Optimism bias | High openness | "This new technology will definitely succeed" | Overconcentration in speculative assets | Portfolio percentage caps |

- Awareness of which biases match your personality profile is the first step toward mitigation.

- Financial advisors who understand their clients' Big Five profiles can design personality-informed planning that explains "irrational" behaviors as personality-driven rationality2.

- For the broader context of how personality shapes all types of decisions, see our decision-making styles guide.

Personality and Debt Management

Credit card debt, loan default risk, and emergency fund preparedness all show personality-trait correlations after controlling for income and demographics.

| Financial Outcome | Key Trait Correlation | Demographic Controls | Probability Shift |

|---|---|---|---|

| Revolving credit card debt | Low conscientiousness | Age, income controlled | Plus 7.7 percentage points3 |

| Emergency expense coverage | High conscientiousness | Age, income controlled | Significantly higher |

| Loan default risk | Low conscientiousness, high neuroticism | Income, education controlled | Elevated |

| Savings account holding | High conscientiousness | Demographics controlled | Significantly higher |

| Overuse of buy-now-pay-later | Low conscientiousness, high extraversion | Age controlled | Elevated |

- The Federal Reserve Bank of Boston found that after controlling for demographics and income, personality traits were not significant predictors of bank account or credit card holding in regression models. However, they were significant for debt revolving behavior, suggesting traits matter most in ongoing financial management rather than product acquisition3.

- This is an important nuance: personality predicts how you manage money more than whether you have financial products.

Building a Personality-Informed Financial Plan

Understanding your Big Five profile enables a tailored financial strategy that works with your natural tendencies rather than against them.

| Your Trait Profile | Core Financial Risk | Priority Strategy | Implementation Tool |

|---|---|---|---|

| High conscientiousness | Under-risking (too conservative) | Ensure growth allocation matches time horizon | Target-date retirement funds |

| Low conscientiousness | Impulse spending, under-saving | Automate everything possible | Auto-transfers, spending alerts |

| High neuroticism | Panic decisions, avoidance | Pre-committed investment policy statement | Written plan reviewed quarterly |

| Low neuroticism | Insufficient caution | Maintain emergency fund, review insurance | Annual risk assessment |

| High extraversion | Overtrading, social-driven choices | Trade limits, systematic rebalancing | Automated portfolio management |

| High openness | Overconcentration in speculative assets | Cap alternative investments | Percentage-based allocation rules |

| High agreeableness | Under-growth, lending beyond means | Growth allocation, personal lending limits | Separate "lending" budget line |

Financial action checklist by personality

- Take a validated Big Five assessment to identify your dominant financial personality traits.

- Match your profile to the risk and strategy tables above.

- Automate at least one financial behavior (savings transfer, bill payment, or rebalancing).

- Identify your top two cognitive biases from the bias table and set up countermeasures.

- Schedule quarterly financial reviews regardless of personality type.

- If high in neuroticism, write an investment policy statement when calm and refer to it during market volatility.

- If high in extraversion, set a monthly maximum number of trades.

- Review this checklist annually and adjust as your financial situation and self-awareness evolve.

FAQ

Which personality trait is the strongest predictor of financial success?

Conscientiousness is consistently the strongest predictor of positive financial outcomes across multiple studies. It drives disciplined spending, consistent saving, higher net worth, and lower debt. In regression models, conscientiousness carries the highest weight among all Big Five traits for predicting financial literacy and outcomes12.

How does neuroticism affect investment decisions?

Neuroticism promotes risk aversion, preference for safer investments (bonds, savings accounts, guaranteed returns), and avoidance of financial decisions with uncertain outcomes. During market downturns, high-neuroticism investors are more likely to panic sell, locking in losses. However, moderate neuroticism can be adaptive by motivating emergency fund maintenance42.

Why do extraverts tend to overtrade?

Extraversion is linked to overconfidence bias, higher risk tolerance, and susceptibility to social influence. Extraverted investors trade more frequently because they feel confident in their market timing ability and are influenced by investment discussions in their social networks. Higher trading volume is associated with lower net returns due to transaction costs41.

Can personality traits predict credit card debt?

Yes, to a degree. A Federal Reserve Bank of Boston study found that low conscientiousness increases the probability of revolving credit card debt by 7.7 percentage points after controlling for age and income. However, personality traits are not significant predictors of simply holding a credit card. They matter more for ongoing debt management behavior3.

How does openness to experience relate to financial risk-taking?

Openness correlates with higher risk tolerance, interest in novel investments, and early adoption of new financial products. Risk-tolerant groups show mean openness scores of 3.18 on a 5-point scale. The risk is that high-openness individuals may be drawn to speculative or poorly understood investments due to novelty attraction and optimism bias4.

Do personality traits affect financial literacy?

Personality traits both directly affect financial decisions and indirectly affect them through financial literacy. Conscientiousness predicts higher financial literacy through systematic information-seeking. Openness drives curiosity-based financial learning. Neuroticism can create avoidance of financial education. Partial least squares analysis confirms that traits mediate the personality-to-financial-decision pathway1.

Can a financial advisor use personality data to improve advice?

Yes. Research from the University of Georgia specifically recommends incorporating personality assessment into financial planning. Understanding a client's Big Five profile helps advisors explain "irrational" behaviors as personality-driven patterns, design strategies that work with natural tendencies, and anticipate likely biases during market volatility2.

Are personality-finance links the same across income levels?

No. Research shows that trait influence varies by income bracket. Among higher-income earners, agreeableness is more prevalent and drives security-focused decisions. Financial literacy mediates the effect differently across income levels, and demographic controls (age, education, urban versus rural) significantly modify trait-outcome relationships13.

Notes

Primary Sources

| Source | Type | Key Contribution | URL |

|---|---|---|---|

| SIB Research (RIJEB) | Peer-reviewed journal | Personality traits, risk tolerance, and behavioral biases | Link |

| Journal of Competitiveness (JOC) | Peer-reviewed journal | PLS analysis of traits, literacy, and investment decisions | Link |

| University of Georgia (FSR) | Peer-reviewed journal | OCEAN model and financial success prediction | Link |

| Federal Reserve Bank of Boston | Working paper | Personality traits and debt management, demographic controls | Link |

| Emerald Insight (IJBM) | Peer-reviewed journal | Investment intention and financial satisfaction | Link |

Conclusion

Your personality traits create financial tendencies, not financial destinies. Conscientiousness drives wealth through discipline, neuroticism creates protective but growth-limiting caution, extraversion fuels action but invites overconfidence, openness enables innovation but courts speculation, and agreeableness prioritizes security over maximization.

The practical takeaway is straightforward: identify your dominant traits, recognize the biases they produce, and build systems that compensate for your blind spots. Automated savings for the less conscientious, pre-written investment policies for the neurotic, and trade limits for the extravert are not personality changes. They are environment designs that produce better outcomes regardless of temperament.

Footnotes

-

Journal of Competitiveness (JOC). Big Five personality traits, financial literacy, and investment decisions. C Journal, 539. Available at: https://www.cjournal.cz/files/539.pdf ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10 ↩11 ↩12

-

Nabeshima, G. & Seay, M. (2023). OCEAN: How does personality predict financial success? Family and Consumer Sciences Research Journal, University of Georgia. Available at: https://openjournals.libs.uga.edu/fsr/article/download/3178/3113/9873 ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

Burke, J. et al. (2023). Personality traits and financial outcomes. Working Paper 23-04, Federal Reserve Bank of Boston. Available at: https://www.bostonfed.org/-/media/Documents/Workingpapers/PDF/2023/wp2304.pdf ↩ ↩2 ↩3 ↩4 ↩5 ↩6

-

SIB Research (RIJEB). Influence of personality traits on financial risk tolerance and behavioral biases. Review of Integrative Business and Economics Research, 12(2), 235–251. Available at: https://sibresearch.org/uploads/3/4/0/9/34097180/riber_12-2_19_t23-044_235-251.pdf ↩ ↩2 ↩3 ↩4 ↩5 ↩6 ↩7 ↩8 ↩9 ↩10

-

Emerald Insight (IJBM). The influence of personality traits on investment intention and financial satisfaction. International Journal of Bank Marketing, 41(4), 810. Available at: https://www.emerald.com/ijbm/article/41/4/810/510198/The-influence-of-personality-traits-on-investment ↩ ↩2